Although you don’t hear this question–or even the phrase–very often anymore, it’s still an important factor in managing your checking account. According to StatisticBrain.com, 79 percent of us never, or rarely, balance our checkbook. What “balancing” means is that you compare your records to those of the bank and make sure that the two figures agree. The important phrase in that sentence is “your records.” If you do not maintain your own records and receipts of transactions on your checking account, there will be no way to discover, or prove, an error if you feel there is a discrepancy in your balance. If you’re managing your account by checking your balance each day, and then spending based on what you see, then it’s just a matter of time until you get burned.

I have worked in banking for over 25 years and have heard various excuses for customers not completing this important task: I always keep a little extra money in my account, just in case, to be sure there’s not a problem. Or, I check my account every day so I know how much I have. Or–my favorite–banks don’t make mistakes.

Guess again. Banks do make mistakes. And the sooner you catch one, and can provide backup documentation, the more likely it will be resolved in your favor. A transaction may post twice, or for a wrong amount. A deposit could go missing. Having a receipt for these issues is ideal, but even without a receipt, if you have recorded the date and amount of the transaction in your own records, the bank will at least have a starting point to start researching your transaction.

Another important reason to monitor and balance your account: Fraud. Comparing every transaction on your account to your own records means you’ll spot unauthorized transactions and ID theft right away, and the sooner you report suspected fraud the more likely you are to get that money back. It’s not enough to just give your transactions a quick look-over. Let’s say you are a subscriber to netflix. You see your monthly fee hit your account and think, okay, that’s me. Now suppose a netflix debit posts again in 3 weeks. Will you immediately realize that that might be a fraudulent transaction, or will you just think, oh, okay, netflix time again. If you’re balancing your checkbook you’ll notice right away that that second fee might not be legitimate. I often have customers come to see me with a fraudulent transaction that is some type of membership fee and they don’t even realize that that charge has been posting to their account for the past 6 months. Perhaps they recognized the vendor’s name as one they sometimes use, or maybe they weren’t looking closely enough. They certainly weren’t balancing. Unfortunately, most banks policies cite 60 days as the time frame to file a dispute. So if it’s been 6 months, you may be out of luck in getting back some of these charges.

A third reason to balance your account: You do not want to pay overdraft fees! Making sure the bank agrees with what you think is your account balance is the best way to avoid an overdrawn account. If you write a check, and you aren’t keeping records, you may forget about it. Charitable organizations and the IRS are notorious for holding these items for a while before depositing or cashing them. I still have customers who will come in and say, “I can’t be overdrawn, my balance was ______ just yesterday!” Upon looking, I see a transaction that posted overnight. “Oh.” They tell me. ” I thought that already cleared.” You would know it had not cleared if you were balancing.

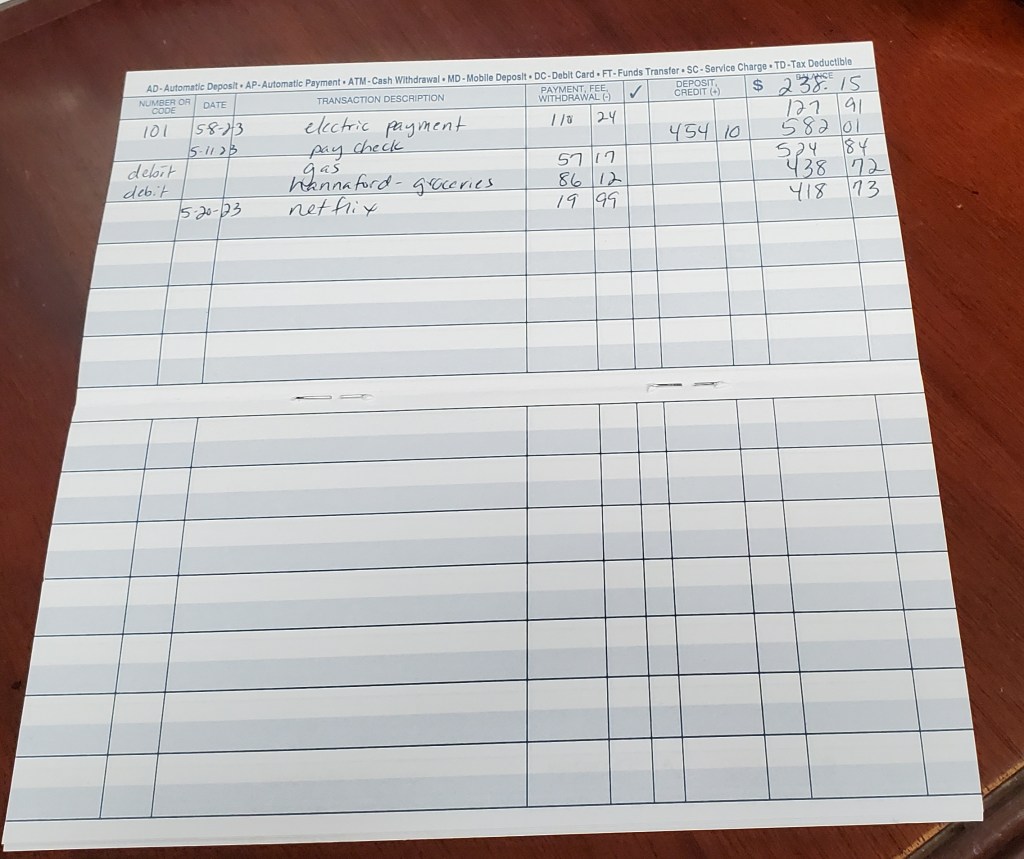

So I keep talking about your records. The most common type of record is a transaction register. If you don’t have one, you can visit your bank and they will provide you with one. Here is what it looks like:

And here is what it looks like when it’s partially completed.

Historically, before online banking and apps and maybe even before debit cards, balancing your checkbook worked like this:

- You received your monthly statement in the mail

- You compared all of the transactions on your statement with your transaction register and marked them off in the register to signify that the amounts agreed and that they had cleared your account

- You completed a form provided with your statement and filled in the following items: the ending balance from your statement, the items that were still outstanding (those that you have authorized to come out of your account but you do not yet see on the history and/or statement); debit items (checks, automatic withdrawals and debit card purchases) go in one section and credits (deposits) go in a second section.

- You did the math: you start with your statement ending balance, subtract any debits that you’ve made that do not appear on the statement and add in the credits that you’ve made that do not appear on your statement; the figure you end up with after these calculations should agree to the ending balance you have in your manual records (transaction register). This form looks something like this:

If the two figures did not agree, you would double check that the items you recorded were the same as what appeared on your statement, and also check the calculations in your register to be sure you didn’t make a mathematical error. Theoretically, once you’ve accounted for outstanding items, your checkbook register and the bank balance should agree exactly.

So what has changed?

First, checks have become fewer. Twenty years ago, when checks were still a main source of payment, it could take a few days to weeks before the recipient of your payment deposited your check and it cleared your account. If you weren’t keeping track, you could look at your balance and think you had much more money than you actually did. With online portals for payments and debit card transactions, this waiting time has all but disappeared. These days you see many of your transactions the next day, same day, or possibly immediately. But not all. These are some of the types of debits that do not always post immediately, and can cause problems if you aren’t maintaining your own records:

- A debit card purchase that has not yet posted: You have probably seen this already. Gas stations, restaurants, and online retailers often don’t post immediately

- Checks

- Monthly automatic items

Second, online banking and apps make it much easier to view your transactions and keep an eye on your balance. The “balancing” you do now could be as simple as taking the current balance that you see online and subtracting any items you know will be coming out, but have not yet, and adding in deposits you aren’t yet seeing, to be sure your records mirror the banks. You can certainly accomplish that without completing a reconciliation form, but you still can’t do it without your own transaction records.

If you’re not a fan of paper records, electronic registers are readily available. Apps like Rocket Money and Volkron will help you track transactions and also monitor your automatic monthly debits as well as helping you budget and track expenses. Clearcheckbookonline.com is another free tool for keeping an eye on your outstanding transactions and also incorporates budgeting tools and gives you the ability to set reminders for recurring transactions.

When should you get started? Right now! If you haven’t been keeping records, start with the “bank” balance as your starting register balance and begin by recording your automatic monthly transactions, including recording your actual balance, which may differ from the current bank balance. How often should you do the actual balancing? You can do it daily if you feel you need to, but generally once a month is a good way for you to check in and make sure things are going smoothly.

If all this seems a little overwhelming, you can visit your bank and sit down with someone who will be happy to show you how to do it. Believe it or not, your local banker is very happy to help you avoid a situation with overdraft fees, fraud or mistakes on your account. And I think we all want to avoid those!